Labor compliance costs are usually decided long before the first certified payroll is filed. Across infrastructure, renewable energy, and affordable housing projects, labor compliance costs increase when funding triggers prevailing wage requirements, fringe benefit obligations, apprenticeship rules, wage determinations, and recordkeeping requirements that were not fully priced at bid time.

Federal Davis-Bacon rules apply to many federally funded or assisted construction contracts over $2,000. HUD programs such as HOME and CDBG carry their own labor standards triggers, while clean energy tax incentives under the Inflation Reduction Act can increase credit value fivefold when prevailing wage and apprenticeship requirements are met.

State prevailing wage laws administered by agencies such as Oregon BOLI and California DIR can layer on top of federal requirements. As a result, labor compliance costs often depend less on the project type and more on the funding structure, labor standards, and reporting obligations attached to the project.

Why Labor Costs Move Before Work Starts

Contractors often think compliance shows up as paperwork. In reality, it shows up first in estimating. A prevailing wage obligation is not just a wage issue; it is the combination of base hourly rates, fringe benefits, worker classification rules, apprentice utilization rules, certified payroll reporting, and retention of payroll records. DOL guidance is explicit that prevailing wage includes both the basic hourly rate and fringe benefits, that the proper wage determination must be included in bid documents and contracts, and that certified payrolls are generally submitted weekly on Form WH-347 or an equivalent format.

For contractors operating across states, the picture gets more expensive when state law applies independently. State agencies such as BOLI in Oregon and DIR in California define prevailing wage separately for covered public works projects, and both emphasize that rates are tied to classification and include fringe value. That means the same crew can carry different labor costs depending on funding source, geography, and trade assignment.

Infrastructure Projects

Infrastructure projects are usually the most predictable from a compliance standpoint because public funding and public works status are often visible early. Federal Davis-Bacon and Related Acts apply to many federally funded or assisted contracts over $2,000 for the construction, alteration, or repair of public buildings or public works, and state public works laws can add a separate layer of rates and reporting.

Where labor costs typically rise on infrastructure work:

- Higher minimum wage rates tied to federal or state wage determinations

- Fringe benefit obligations that must be paid in cash or through bona fide plans

- Weekly certified payroll preparation and review

- Multiple classifications on one project, especially for utilities, site work, paving, concrete, and specialty trades

- Greater prime-contractor oversight of subcontractor payroll and documentation

The hidden margin loss rarely exists in the existence of the prevailing wage itself. It is misclassification, outdated wage determinations, or late discovery that a state public works rule also applies. DOL stresses that contractors need the correct wage determination in the bid package so labor can be priced accurately from the start.

Renewable Energy Projects

Renewable energy projects are often the least predictable because many begin as private developments and then add federal incentives, state programs, or utility-backed funding later in the process. Under IRS and DOL guidance, taxpayers can increase the base amount of many clean energy credits or deductions by five times if prevailing wage and apprenticeship requirements are satisfied. Those rules are separate from Davis-Bacon enforcement, but they still rely on Davis-Bacon wage rates, and state or local wage laws may still apply at the same time.

Where labor costs typically rise on renewable projects:

- Prevailing wage assumptions tied to enhanced IRA credit value

- Registered apprenticeship hour requirements and ratio management

- Specialized classifications for electrical, transmission, battery storage, and energy-adjacent scope

- Additional recordkeeping is needed to support tax credit claims

- Rework when subcontractors price the job like private commercial construction instead of compliance-based construction

This is where compliance becomes a finance issue, not just a payroll issue. If labor standards are missed, the project may face cure payments, penalties, or a reduced credit position. The result is immediate pressure on margin, especially when the original pro forma assumed enhanced tax credit value.

Affordable Housing Projects

Affordable housing is the most funding-sensitive project type. Labor costs often change after financing is assembled, not before, because projects can combine HOME funds, CDBG funds, local subsidy, tax-credit equity, and private debt. HUD states that Davis-Bacon applies to contracts covering the construction of affordable housing with 12 or more HOME-assisted units, and once triggered, it applies to the entire project covered by that construction contract. HUD guidance also explains that CDBG applies Davis-Bacon labor standards to construction, alteration, or repair work over $2,000 financed in whole or in part with CDBG or other federal funds.

Where labor costs typically rise in affordable housing:

- Funding-stack changes that trigger prevailing wage after early budgeting is done

- Wage determinations and classifications that were not built into the original GMP or subcontractor pricing

- Weekly payroll administration and owner or agency reporting

- State prevailing wage overlap on public or publicly assisted portions of the work

- Documentation pressure during draws, monitoring, or closeout

Affordable housing teams get into trouble when they assume the building type controls labor standards. HUD’s own guidance shows it is the assistance structure and contract arrangement that often control the answer.

Practical Controls That Protect Margins

The most effective contractors treat compliance as a preconstruction cost-control system, not a back-office cleanup exercise. A strong process usually includes:

- Map every funding source before bid day

- Confirm whether federal, state, local, or tax-incentive labor standards apply

- Lock the correct wage determinations and classifications before subcontracts are signed

- Verify apprentice registration and applicable ratios before apprentices start work

- Build a weekly payroll review into project controls, even if the owner reviews less often

- Retain payrolls, classifications, fringe support, and apprentice records in one audit-ready file for at least three years after completion when federal construction labor standards apply

These steps are what connect this topic to a broader state- and industry-specific compliance pillar. The laws vary, but the margin-protection pattern is consistent: identify the trigger early, price the labor correctly, and keep the documentation tight.

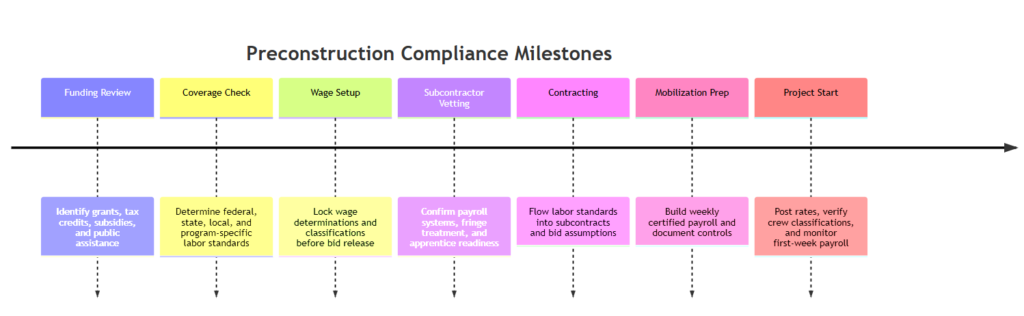

Preconstruction Compliance Timeline

The milestones below reflect the sequence most project teams should follow before mobilization, based on DOL, HUD, IRS, and state-agency guidance on coverage, wage determinations, apprenticeship, payroll, and record retention.

Conclusion

Compliance does not just affect labor costs after the job starts. It changes labor cost when funding is structured, when wage determinations are selected, when apprentices are staffed, and when subcontractors are onboarded. Infrastructure projects are usually the clearest, renewable energy projects are often the most financially sensitive, and affordable housing projects are the most vulnerable to funding-trigger surprises. The contractors who stay profitable are the ones who turn compliance into a front-end planning discipline. If your team is bidding work with public funds, tax incentives, or layered housing finance, schedule a working session with Prevailing Wage Consulting before labor assumptions become expensive corrections.